All Categories

Featured

Table of Contents

- – Health Insurance Plans For Family Stanton, CA

- – Harmony SoCal Insurance Services

- – Planning Life Insurance Stanton, CA

- – Best Individual Health Insurance Plans Stanton...

- – Blue Cross Blue Shield Health Insurance Plans...

- – Best Individual Health Insurance Plan Stanton...

- – Blue Cross Blue Shield Health Insurance Plan...

- – Family Plan Life Insurance Stanton, CA

- – Seniors Funeral Insurance Stanton, CA

- – Health Insurance Plans For Family Stanton, CA

- – Affordable Life Insurance Plans Stanton, CA

- – Life Insurance Family Plan Stanton, CA

- – Family Health Insurance Plans Stanton, CA

- – Harmony SoCal Insurance Services

Health Insurance Plans For Family Stanton, CA

Harmony SoCal Insurance Services

2135 N Pami Circle Orange, CA 92867(714) 922-0043

https://maps.google.com/maps?ll=33.823884,-117.830838&z=16&t=h&hl=en&gl=US&mapclient=embed&cid=276141583131225364

Questions? We enjoy to assist you every action of the way.

Due to the fact that there are various types of health insurance, you ought to make sure to look for the one that fits your needs. Thorough medical insurance provides advantages for a broad variety of wellness care services. These health strategies offer a breakdown of wellness advantages, might limit your prices if you obtain services from among the service providers in the plan's network, and normally call for co-payments and deductibles.

Planning Life Insurance Stanton, CA

You are only covered if you obtain your treatment from HMO's network of suppliers (other than in an instance of emergency). With many HMO plans you pay a copayment for every protected service. You pay $30 for a workplace check out and the HMO pays the remainder of the cost.

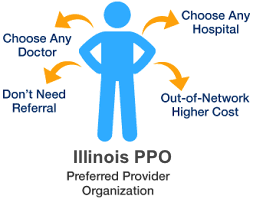

These strategies have a network of favored service providers that you can make use of, however they also cover solutions for out-of-network companies. PPP's will certainly pay even more of the price if you make use of a provider that is in the network. Instance: After copays and deductibles, the plan pays 100% of a solution for a network service provider however 80% for an out-of-network (OON) service provider.

Significant medical plans normally cover medical facility and medical expenses for a mishap or ailment. Example: the plan pays 80% of your hospital stay and you pay the various other 20%.

Whether you choose a major clinical strategy, an HMO or a PPP, your plan will probably have some "cost-sharing" functions. This means that you share the price of care by paying component of the fee for each solution and the insurance provider pays the remainder. Choose a plan that works ideal with the kind of health and wellness insurance you think you will make use of.

Best Individual Health Insurance Plans Stanton, CA

Example, you pay $30 for a workplace check out and the plan pays the remainder. A Plan may have various copayments for different kinds of solutions. The copayment for a medical care visit might be $30 and copayment for an emergency clinic check out might be $150. An insurance deductible is the amount you pay before the plan begins to spend for many covered services.

You pay a $2,500 deductible towards your health care services yearly before the plan pays any Coinsurance is a percent of the enabled charge that you spend for a protected solution advantages. Coinsurance is a percent of the enabled fee that you spend for a protected solution. You pay 20% of the price of a covered office go to and the plan pays the remainder.

Blue Cross Blue Shield Health Insurance Plans Stanton, CA

The plan may enable just 10 brows through to a chiropractic specialist. The strategy might leave out (not pay for) cosmetic surgical treatment, and you will pay for the whole price of service.

There are many different means that you can buy a health plan in Massachusetts. Several people obtain their wellness strategy with their place of work.

Best Individual Health Insurance Plan Stanton, CA

You can pick the health insurance plan that is finest for you from the choices used. If you are signed up as a student in a Massachusetts university or college, you can buy a health insurance via your college. This SHIP id created for pupils and is just offered while you are registered.

And the company can not turn you down if you have a health condition. Sometimes the company will route you to acquire their health insurance via an intermediary. An intermediary is a firm that cares for the registration and costs. If you satisfy certain revenue requirements, you might be qualified for MassHealth.

Blue Cross Blue Shield Health Insurance Plans Stanton, CA

You can find out more at or call 1-800-841-2900 If you do not function for an employer that pays at the very least 33% of your health insurance plan costs, you may be able to purchase a health insurance plan from the Port. These are strategies used by Massachusetts HMOs that the Connector has chosen to have great worth.

The state and federal government supply reduced cost health protection for specific people through public wellness programs. When picking a health and wellness strategy, it is crucial to take into consideration the differences in between your alternatives.

Buying medical insurance can be overwhelming, but remember, if the plan seems too great to be real, it possibly is. Do deny a discount rate strategy as an option to health insurance coverage. Price cut strategies bill a month-to-month charge for access to healthcare services at a decreased fee.

There are not specific customer protections that apply to these strategies. They may not guarantee any type of payments, and they do not always pay costs for the very same kinds of services that health and wellness insurance covers.

Family Plan Life Insurance Stanton, CA

In this way you can see in advance if the plan is appropriate for you and your household. Ask what advantages the strategy does and does not cover, what advantages have limitations; ask whether the strategy covers your prescription drugs; ask where you can view a list of the healthcare suppliers in the plan's network.

High out-of-pocket prices can soon wipe out the savings of reduced month-to-month premiums. You need to ask what is the monthly costs you would certainly pay for the strategy, what out-of-pocket costs will certainly you have and whether there is an optimum, and what is the deductible. Do not be tricked by phony health insurance marketing on the net or through unsolicited faxes or telephone call.

Testimonial any site very carefully and search for disclaimers such as "this is not insurance coverage" or "not readily available in Massachusetts." Be careful of marketing that does not offer the particular name and address of the insurance firm using the health insurance. If the customer is unwilling to supply the precise name of the company, his/her name, where the business lies, or whether the company is accredited, or if they are a licensed insurance agent, you must simply hang up.

Seniors Funeral Insurance Stanton, CA

You do never need to give monetary information to get a quote. Be careful of high pressure sales techniques that tell you a low month-to-month cost is a restricted time offer and will certainly run out in a day or 2. There is no such point as a minimal time deal or "unique" in medical insurance.

When you do locate a health insurance that looks like it satisfies your requirements, check the Department of Insurance policy web site or contact us to find out if the company is licensed to market that kind of insurance policy in Massachusetts before you commit to purchasing the item. Be cautious not to offer out individual details or make a payment in action to an unrequested fax or without examining it out first.

You have choices when you go shopping for health and wellness insurance. If you're acquiring from your state's Industry or from an insurance broker, you'll select from health insurance plan arranged by the level of advantages they provide: bronze, silver, gold, and platinum. Bronze plans have the least protection, and platinum strategies have one of the most.

Health Insurance Plans For Family Stanton, CA

Exactly how are the strategies different? In enhancement, deductibles-- the amount you pay before your plan pays any of your health care expenses-- differ according to plan, generally with the least expensive lugging the highest insurance deductible.

If you see a medical professional who is not in the network, you might need to pay the full expense yourself. Emergency solutions at an out-of-network healthcare facility have to be covered at in-network prices, however non-participating medical professionals that treat you in the healthcare facility can bill you. This is the expense you pay monthly for insurance.

A copay is a level fee, such as $15, that you pay when you obtain treatment. These costs differ according to your strategy and they are counted toward your insurance deductible.

Greater out-of-pocket prices if you see out-of-network physicians vs. in-network providersMore documents than with various other plans if you see out-of-network providers Any kind of in the PPO's network; you can see out-of-network doctors, but you'll pay even more. This is the price you pay each month for insurance. Some PPOs might have an insurance deductible.

Affordable Life Insurance Plans Stanton, CA

A copay is a flat charge, such as $15, that you pay when you obtain treatment. Coinsurance is when you pay a percentage of the costs for treatment, for instance, 20%. If your out-of-network medical professional charges even more than others in the location do, you might need to pay the balance after your insurance policy pays its share.

If you utilize an out-of-network provider, you'll need to pay the company. You have to submit a claim to get the PPO strategy to pay you back. With an EPO, you may have: A modest quantity of freedom to choose your health and wellness care companies-- greater than an HMO; you do not have to obtain a referral from a medical care doctor to see an expert.

Reduced premium than a PPO offered by the exact same insurerAny in the EPO's network; there is no protection for out-of-network carriers. This is the expense you pay every month for insurance coverage. Some EPOs might have a deductible. A copay is a level charge, such as $15, that you pay when you get care.

Life Insurance Family Plan Stanton, CA

If you see an out-of-network service provider you will need to pay the full expense. There's little to no documents with an EPO. A POS plan mixes the attributes of an HMO with a PPO. With POS strategy, you may have: Even more flexibility to pick your health treatment suppliers than you would in an HMOA moderate amount of documentation if you see out-of-network providersA health care medical professional who collaborates your care and that refers you to professionals You can see in-network service providers your health care medical professional refers you to.

Your plan might need you to pay the quantity of a deductible prior to it covers treatment past preventive services. You will pay either a copay, such as $15, when you get treatment or coinsurance, which is a percent of the costs for treatment.

Other than preventive care, you should pay all your prices up to your deductible when you go for clinical care. You can establish up a Wellness Financial savings Account to help pay for your costs.

Go to free of charge, professional assistance getting advantages that are appropriate for you. was created by the Wisconsin Office of the Commissioner of Insurance (OCI) with the Wisconsin Department of Health Services (DHS) and lots of various other partners. We're all committed to helping every Wisconsinite obtain accessibility to affordable wellness insurance coverage.

Family Health Insurance Plans Stanton, CA

Harmony SoCal Insurance Services

Address: 2135 N Pami Circle Orange, CA 92867Phone: (714) 922-0043

Email: [email protected]

Harmony SoCal Insurance Services

What is open enrollment? It's the moment each autumn when you can enlist in medical insurance for the following year. The majority of the moment, you can only sign up throughout open registration. A life occasion (like marrying, having a child, or shedding various other protection) may provide you a special enrollment period.

Term Insurance For Seniors Stanton, CAEstate Planning Life Insurance Stanton, CA

Affordable Life Insurance Plans Stanton, CA

Near Here Seo Marketing Stanton, CA

Around Me Seo Firm Stanton, CA

Harmony SoCal Insurance Services

{kind=link}

Table of Contents

- – Health Insurance Plans For Family Stanton, CA

- – Harmony SoCal Insurance Services

- – Planning Life Insurance Stanton, CA

- – Best Individual Health Insurance Plans Stanton...

- – Blue Cross Blue Shield Health Insurance Plans...

- – Best Individual Health Insurance Plan Stanton...

- – Blue Cross Blue Shield Health Insurance Plan...

- – Family Plan Life Insurance Stanton, CA

- – Seniors Funeral Insurance Stanton, CA

- – Health Insurance Plans For Family Stanton, CA

- – Affordable Life Insurance Plans Stanton, CA

- – Life Insurance Family Plan Stanton, CA

- – Family Health Insurance Plans Stanton, CA

- – Harmony SoCal Insurance Services

Latest Posts

Ranchita Companion Senior Care

Home Health Care Business Pioneertown

Home Healthcare La Quinta

More

Latest Posts

Ranchita Companion Senior Care

Home Health Care Business Pioneertown

Home Healthcare La Quinta